Investments

At GSI we take evidence from academic research in financial markets and translate it into sensible investment strategies.

PLEASE NOTE: From 28 April 2025, GSI fund names were updated to align with EU ESG naming guidelines:

Global Sustainable Value Fund → Global Aware Value Fund

Global Sustainable Focused Value Fund → Global Aware Focused Value Fund

There are no changes to the investment strategy, objectives, or SFDR Article 8 classification.

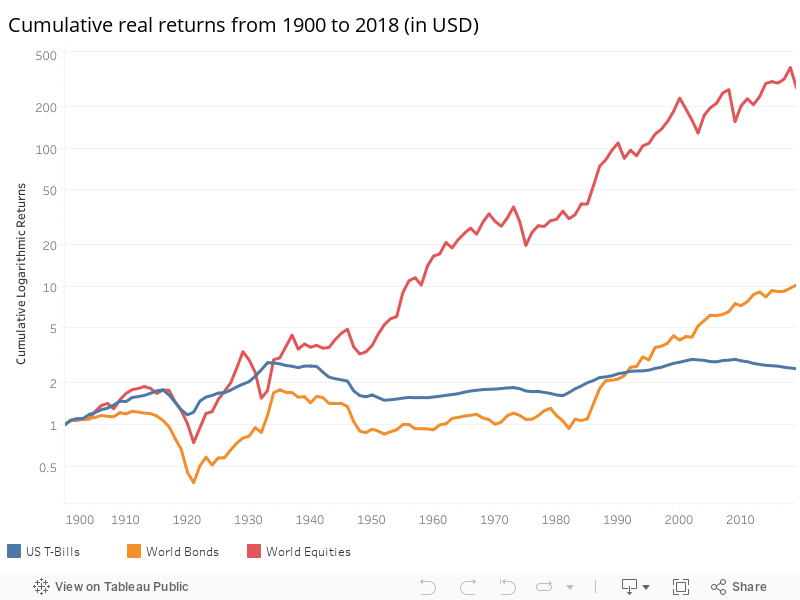

A long-term view of investing

Stock market history shows us that investors are rewarded for bearing the risk of investing in equities over bonds, and bonds over inflation, in the long-term. Markets reward investors that are prepared to be exposed to the risk of loss. This is a key principle of well-functioning markets and one that investors can use to their advantage. To benefit from these returns, investors must stick with the market and stay invested – especially during times when it may feel uncomfortable to do so.

The long run return over inflation of global equities and bonds.

Source: Elroy Dimson, Paul Marsh and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research. Copyright © 2019 Elroy Dimson, Paul Marsh and Mike Staunton

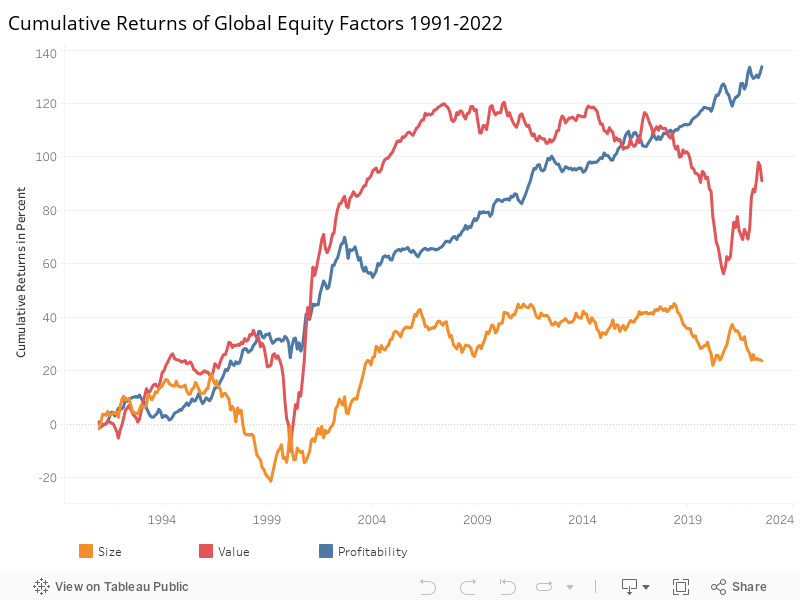

The importance of factors

Academic researchers have identified common underlying patterns in stock returns, known as ‘factors’. Over the long-term, portfolios built using these factors can deliver higher returns than market-weighted indices. These factors are persistent over time, cost-effective to capture and prevalent across markets. They include:

– Size factor – smaller company stocks that generate higher returns than larger companies.

– Value factor – stocks trading at lower prices that produce higher returns compared to stocks trading at higher prices.

– Profitability factor – companies generating higher profits, on average, will generate higher returns.

The long run returns of the Fama-French factors for size, value and profitability.

Source: Professor Ken French data library

Previously, factor investing was restricted to institutional investors. Now with improvements in technology and wider access to data, factor investing can be accessed by all types of investor.

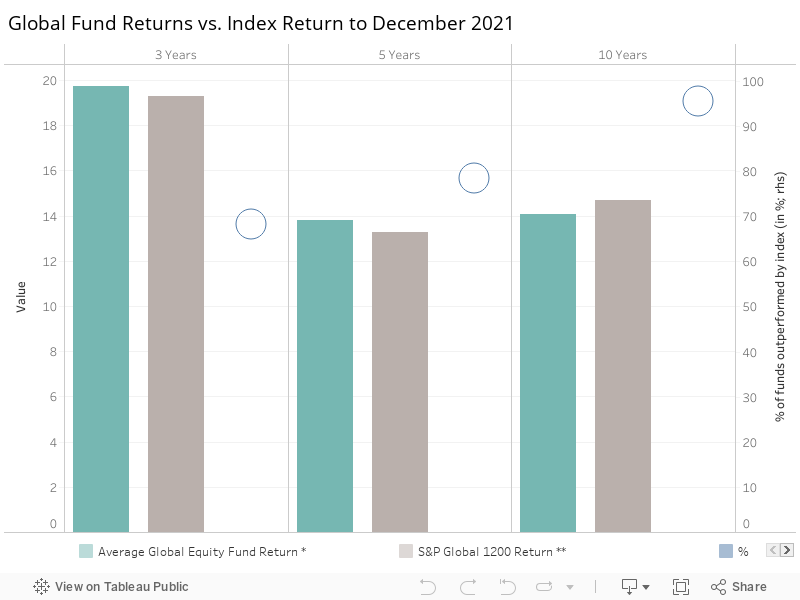

You cannot beat the market, so why try?

The overwhelming evidence from academic research suggests that it is very hard to beat the market once proper adjustments are made for risk. The aggregate activity of competitive investors in the market means that prices absorb information very quickly. Studies of fund returns show that the conventional activity of picking stocks and attempting to time markets to generate returns above the market average is generally a waste of time. Investors are therefore better-served by taking a long-term, systematic approach to investing, while managing their asset allocation and costs.

According to S&P, over 95% of managers of global equity funds fail to match the returns of a global equity index over the 10-year period, to the end of 2021.

Comparison of global manager returns vs. index over 10 years.

* Asset weighted average performance of global equity funds available to UK investors.

** Percentage of global equity funds outperformed by an S&P global large-cap index.

Source: SPIVA Europe report, December 2021.

“Past performance does not help investors identify funds that are likely to outperform in the future, mainly because the majority of firms do not persistently outperform”

FCA Asset Management Market Study, Interim Report, November 2016, p52.

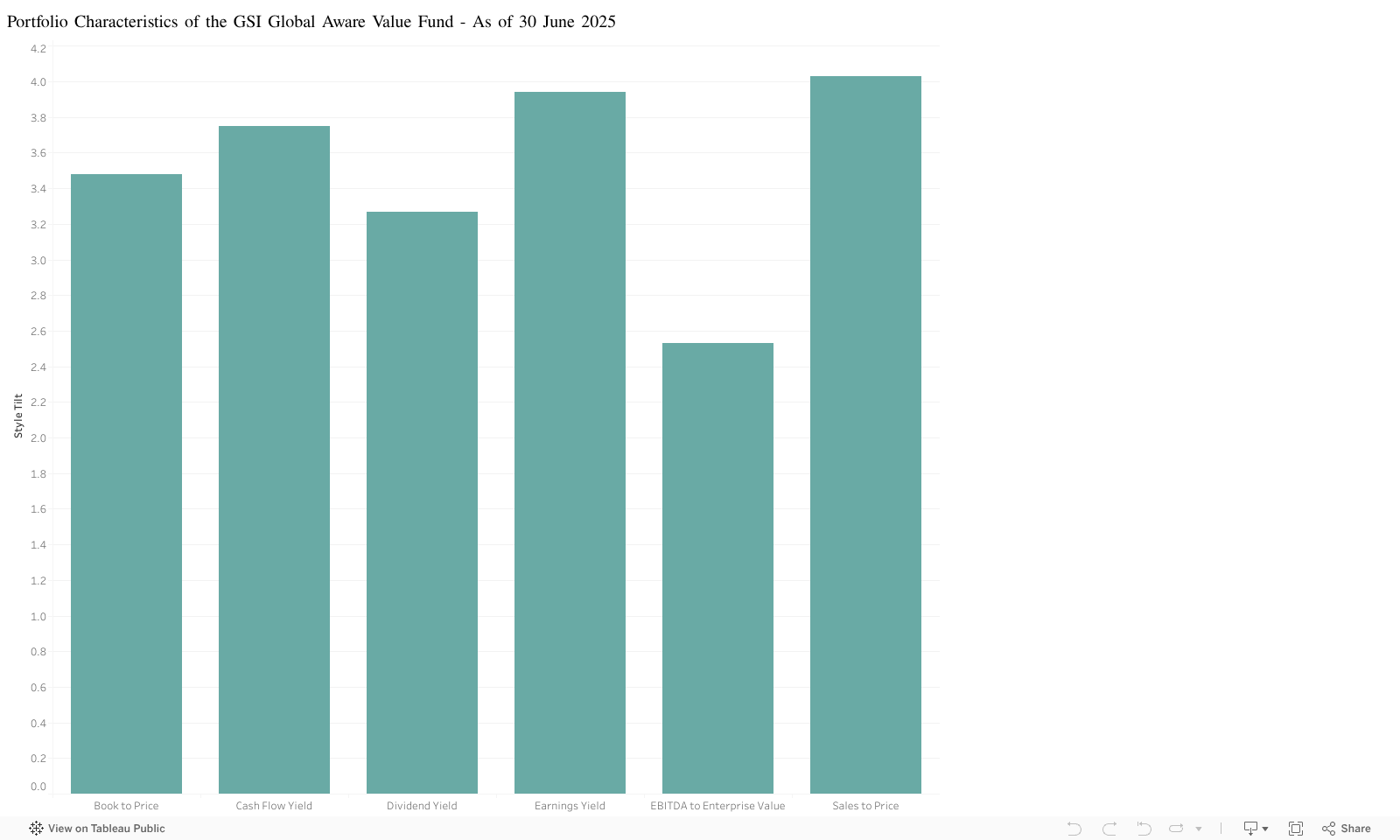

Our portfolio construction

We build portfolios by systematically taking exposure to key factors such as size, value and profitability which, research shows, deliver higher returns in the long-run. We believe that it is essential to maintain diversification across markets, stocks and sectors to reduce downside return risks. By paying more attention to diversification, portfolios can be designed to have better risk/return profiles than market-weighted indices, while preserving high capacity, low turnover and low transaction costs.

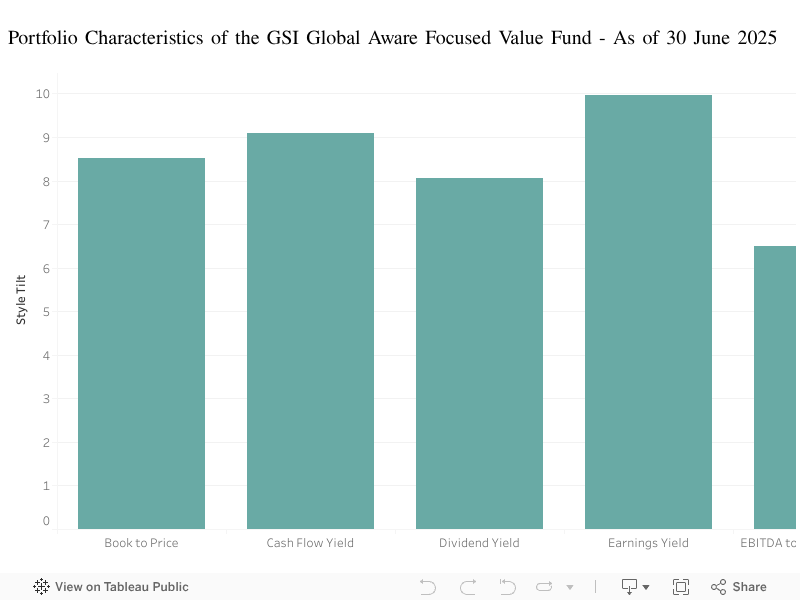

Source: Global Systematic Investors, Style Analytics.

Source: Global Systematic Investors, Style Analytics.